Key takeaway: Three standard scenarios (Central, High, Low) capture the range of plausible outcomes, with battery buildout rates and commodity price assumptions as the primary drivers of revenue divergence. Custom scenarios are also available for bespoke analysis.

Central, low and high scenarios.

Our central scenario is what we consider to be the most realistic worldview. Since the NEM is such a volatile market, we also forecast low and high scenarios to address different risk appetites and capture the range of plausible outcomes.

All three scenarios use the AEMO 2026 Integrated System Plan (ISP) “Step Change” pathway for underlying generation and transmission buildout assumptions. The High and Low scenarios instead diverge from Central through demand-side inputs (data centre demand, EV allocation, and underlying consumption growth), and, for High, a uniform technology cost uplift, higher commodity prices, increased coal outage rates, and lower near-term battery buildout.

High Scenario

Modo Energy forecasts a ‘high’ case, assuming a more optimistic battery revenue scenario.

Battery storage buildout

Battery storage buildout is one of the most important sensitivities to the battery business case, as increased buildout results in a suppressive effect on price spreads. There are currently 21GW of BESS projects in the pipeline that we deem to have made tangible progress, which are aiming to be online by end of 2028. The question is, how many of these projects will be built, and when?

For the high scenario, we have assumed a lower probabilistic total buildout of projects in the pipeline compared to our central scenario, with more and longer delays built into our assumption of when capacity comes online in the near term. We separated battery projects in the pipeline based on project status, and have developed an informed opinion on likely delays and total capacity to come online within each status group based on historical project timelines in the NEM and market expertise, which is indicated in the table below.

Our high scenario has an overall lower battery capacity assumption compared to our central scenario.

Long duration storage project delays

Based on historical trends, we can see that longer duration energy storage will become increasingly important to dampen extreme price peaks, particularly with the increase of solar generation. Therefore, long duration storage project delays will likely have a significant impact on power prices.

For the high scenario, we have assumed a delay of 2 years to the project operational dates for Snowy 2.0 (2030 to 2032), Phoenix Pumped Hydro (2031 to 2033), and Borumba (2035 to 2037).

Demand

Demand is an important sensitivity as it can significantly affect power prices and therefore battery revenue. One of the greatest uncertainties in future demand is data centre buildout, which is forecast using Modo Energy’s own data centre demand model (see Demand).

The High scenario assumes a materially larger data centre build than Central, reaching around 54 TWh NEM-wide by FY2050 versus 36.8 TWh in Central. EV charging demand in the High scenario is allocated using the 2026 ISP’s Accelerated Transition scenario, in place of the Central scenario’s Step Change allocation.

Capex

Capex for a particular technology directly impacts the amount of capacity that can operate economically in the market. A higher capex means fewer batteries are built overall, but also means higher revenues for the battery fleet that is built.

The High scenario applies a uniform 10% uplift to Central technology costs across all generation and storage technologies, including BESS capex. BESS capex continues to be set by Modo Energy’s own market intelligence (refreshed in February 2026) rather than CSIRO GenCost, with the High scenario’s 10% uplift applied on top of that curve.

Commodity prices

Commodity prices impact the cost of operating thermal generators, which in turn impacts their bids into the market. Since most of the electricity generated in the NEM currently comes from thermal generation, even a small percentage change in commodity prices will impact power prices and spreads.

The High scenario assumes commodity prices materially above the central scenario, informed by the historical variability of gas prices (see figure).

Ageing coal and increasing outages

As previously mentioned, thermal generation makes up a large proportion of all electricity generated in the NEM, but this is even more pronounced in New South Wales, Queensland, and Victoria with a majority of generation coming from coal in these states. Therefore, often when there is a significant coal outage (i.e. a forced outage) this causes a period of volatility.

For the High scenario, coal outage rates are assumed to increase year on year, reflecting the historical variability of forced outage rates as plants age toward retirement.

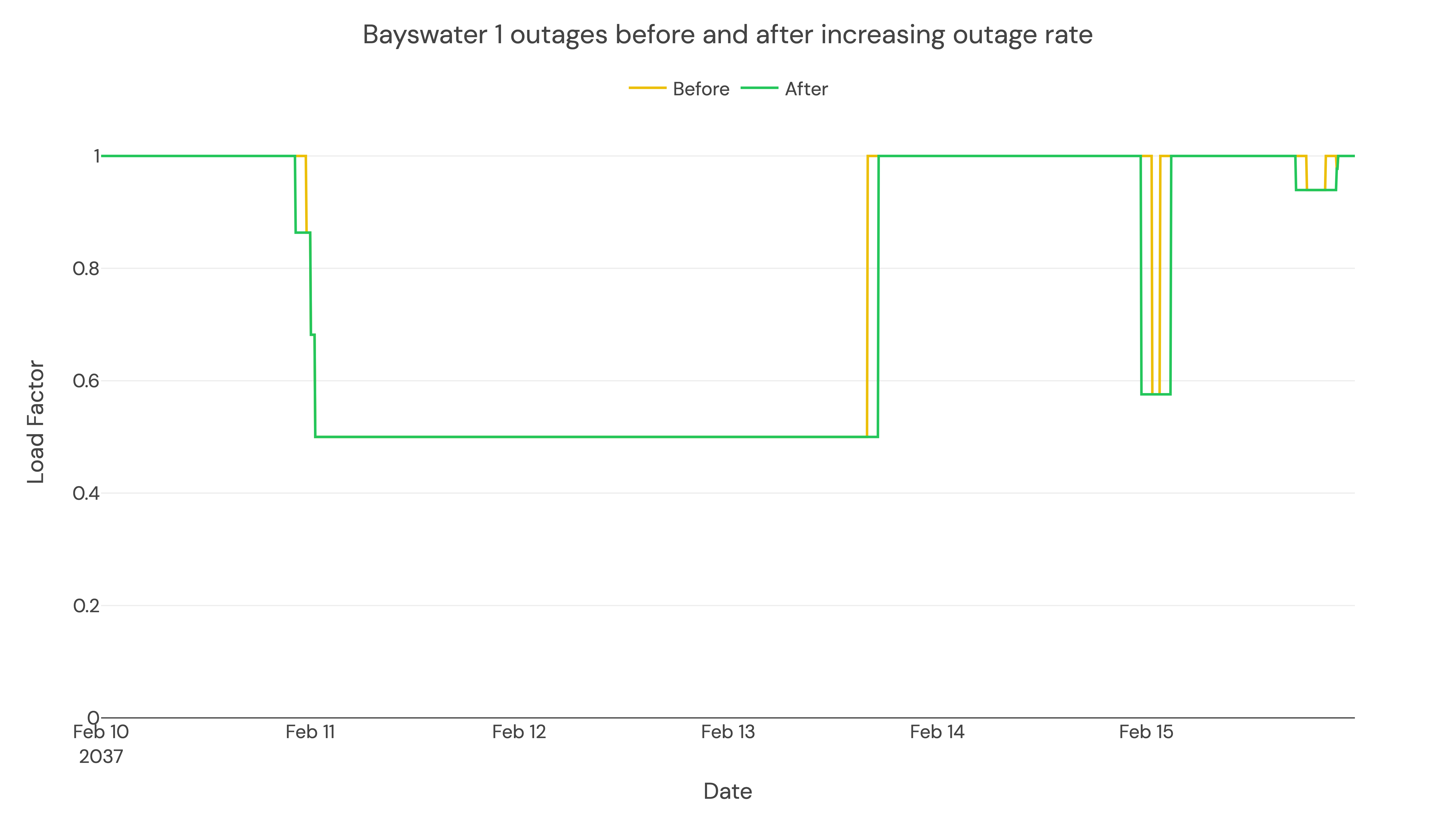

We then extend the existing reference year outages evenly across the year for each generating unit by the number of settlement periods aligning with the increased outage rate for that forecast year.

The chart below demonstrates how this extension is applied on three partial outages for Bayswater unit 1 in 2037.

Low Scenario

Modo Energy forecasts a ‘low’ case, assuming a more conservative battery revenue scenario.

Battery storage buildout

For the low scenario, we have assumed a higher probabilistic total buildout of projects in the pipeline compared to our central scenario. This results in fewer and shorter delays built into our assumption of when capacity comes online, as well as more capacity coming online overall.

Demand

The Low scenario assumes a smaller data centre build than Central, using Modo Energy’s own data centre demand forecast for the Low case. EV charging demand is allocated using the 2026 ISP’s Slower Growth scenario, and underlying consumption growth is scaled to the ESOO Slower Growth demand projection rather than Central’s Step Change projection. Technology costs, including BESS capex, remain the same as Central — the Low scenario diverges only through these demand-side inputs.

Commodity prices

The Low scenario assumes commodity prices below the central scenario, informed by the historical variability of gas prices.

Custom Scenarios

In addition to the three standard scenarios, custom forecast runs can override key input assumptions to create bespoke scenarios tailored to a specific investment thesis or risk assessment. Overridable assumptions include commodity prices, battery buildout rates, demand growth, and capex. This allows users to test sensitivities beyond the range covered by the Central, High, and Low cases. See Running a Forecast for details on how to request a custom run.