Key takeaway: The Capacity Expansion Model co-optimises generation and storage investment from 2030 to 2054, balancing system costs with reliability constraints to produce internally consistent capacity pathways.

Generation capacities and output are modelled using a combination of near-term pipeline data and long-term capacity expansion optimisation.

Capacity Expansion Model

Capacity modelling for the NEM is based on current capacities (from NEM Generation Information), policy assumptions, and Modo Energy’s analysis. Capacity buildout to 2029 is relatively well-defined, with many assets already in the pipeline. For battery storage, Modo Energy’s house view on battery pipeline data is used.

Beyond 2029, long-term generation and storage investment decisions are determined by a Capacity Expansion Model (CEM). The CEM uses an optimisation approach to determine the mix and timing of new capacity that meets system needs while balancing total system cost against reliability requirements.

The CEM spans a planning horizon from 2030 to 2054, producing a coherent long-term capacity pathway. Investment assumptions are sourced from the AEMO ISP 2024 Step Change scenario. Technology costs use the WACC Upper bound scenario from the AEMO ISP to reflect conservative financing assumptions. Investment technologies include Solar PV, Onshore Wind, Offshore Wind, CCGT, OCGT, and Battery Storage (2h, 4h, and 8h durations).

Build limits provide additional guardrails to ensure sufficient firm capacity is built throughout the transition. Technologies such as Offshore Wind, Pumped Hydro, and Reservoir Hydro are treated as policy-led and follow a fixed path informed by external scenarios.

Reliability and investment decisions

The CEM is a capacity expansion model that minimises total system cost - the sum of operational costs, investment costs (capex), and fixed operating costs (opex) - subject to reliability constraints.

Hurdle rates via WACC: Investment costs are annualised using a Capital Recovery Factor (CRF) with technology-specific WACC rates from the AEMO ISP 2024 WACC Upper bound scenario. The WACC effectively acts as a hurdle rate for each technology -the optimiser only builds new capacity if the resulting system cost savings exceed the WACC-adjusted annualised cost of the investment. The WACC rates used are:

| Technology | WACC |

|---|---|

| Solar PV | 10.0% |

| Onshore Wind | 10.5% |

| Offshore Wind | 10.5% |

| CCGT | 13.5% |

| OCGT | 12.0% |

| BESS (all durations) | 11.5% |

Construction-period financing costs are also accounted for using technology-specific lead times and the WACC.

Government policy assumptions

Government policies such as VRET, CIS, LTESA, and SA capacity and firming targets are accounted for in our near term capacity buildout which is based on our battery pipeline, however we are not specifically fixing the model to meet these targets with the exception of Victorian offshore wind policy targets, which are partially met with 2,000 MW built by 2035. Other buildout is economical via capacity expansion.

Minimum synchronous generation constraints

To maintain system security, the model enforces minimum synchronous generation requirements per NEM state, derived from AEMO’s inertia allocations. The effective requirement declines over time as synchronous condensers and grid-forming (GFM) battery storage are deployed, reducing the need for thermal plant commitment to meet inertia needs.

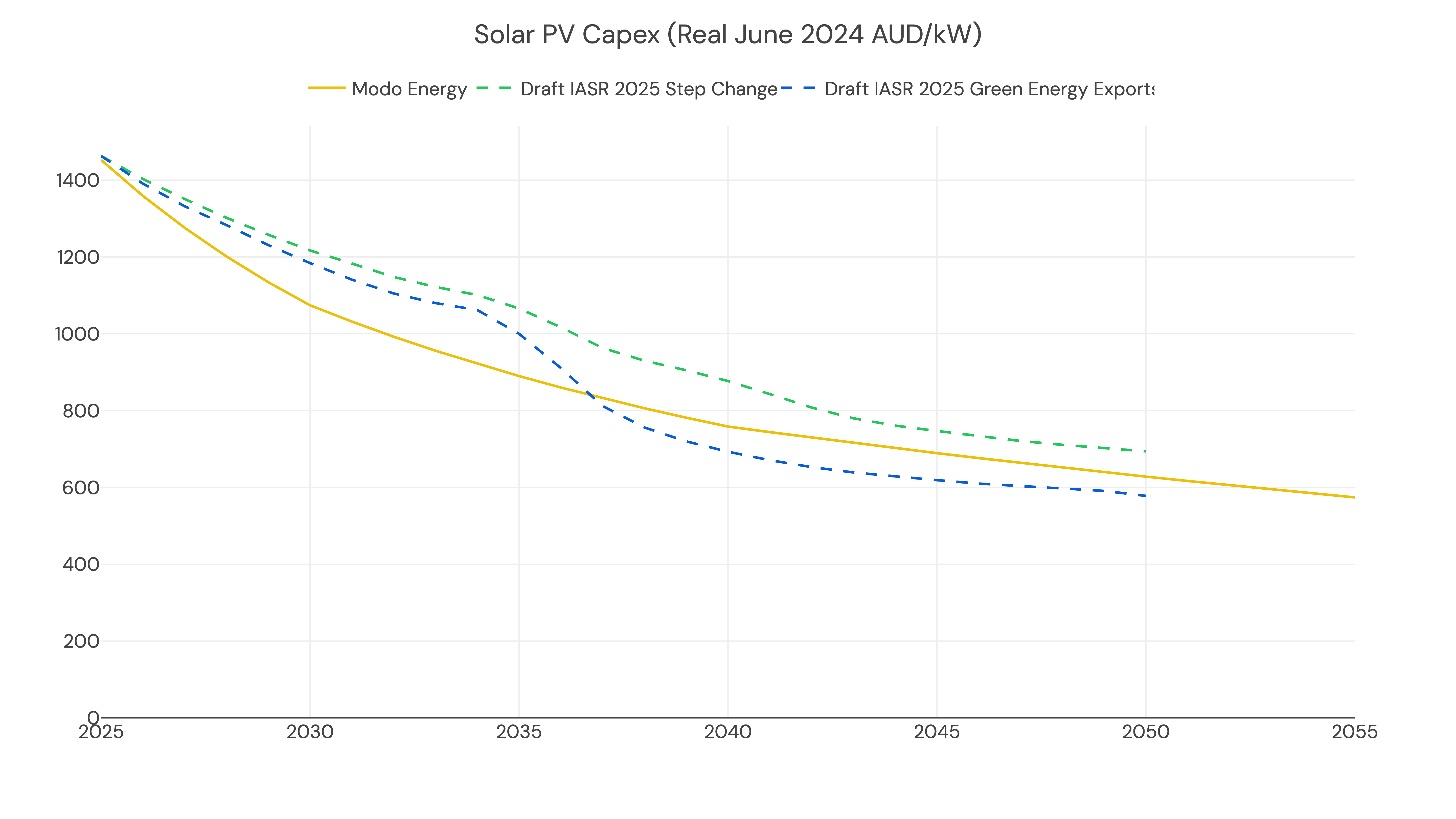

Capex

Capex assumptions for most technologies are sourced from the AEMO Draft IASR 2025. However, a house view is taken on BESS and Solar PV capex based on market research.

Solar PV capex assumptions are based on Modo Energy’s component-level research.

Thermal Generation

Modelling coal, gas, and other thermal generation technologies

Commodity Prices

Gas, coal, and other fuel price assumptions

Renewable Generation

Solar and wind capacity buildout and generation profiles

Reservoir Hydro

Hydroelectric generation and storage modelling

Storage

Battery energy storage system capacity and deployment